View PDF

Overview

IFRS 15 that was issued on 28th of May 2014 provides a single, principles based five-step model to be applied to all contracts with customers. It will improve comparability of reported revenue over a range of industries, companies and geographical areas globally.

IFRS 15 replaces a number of standards and interpretations:

- IAS 11 Construction contracts

- IAS 18 Revenue

- IFRIC 13 Customer Loyalty Programmes

- IFRIC 15 Agreements for the Construction of Real Estate

- IFRIC 18 Transfers of Assets from Customers

- SIC-31 Revenue – Barter Transactions Involving Advertising Services

Objective

The objective is to establish principles that an entity shall apply to report useful information to users of financial statements regarding the nature, amount, timing and uncertainty of revenue, and also cash flows arising from a contract with a customer.

Scope

This new revenue model applies to all contracts with customers except:

If a contract with a customer falls within the scope of both IFRS 15 and the scope of another standard then:

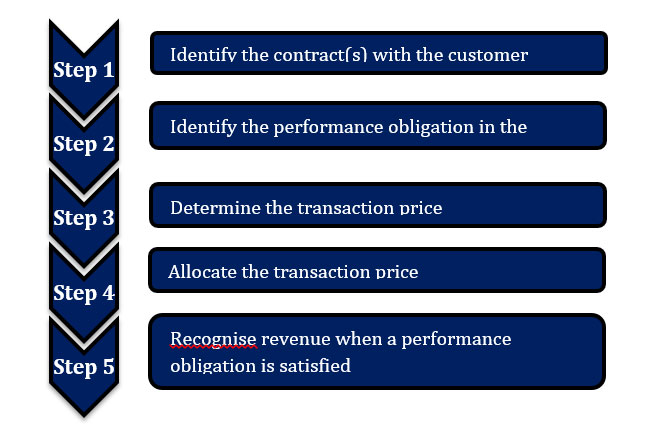

Five-Step Model Framework

The core principle of the standard is that an entity should recognise revenue to show the transfer of promised goods or services to the customer in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

Step 1: Identify the contract(s) with the customer

IFRS 15 defines a contract as an agreement between two or more parties that creates enforceable rights and obligations and sets out the criteria for every contract that must be met.

A contract with a customer will be within the scope of IFRS 15 if all the following conditions are met:

A contract with a customer will be within the scope of IFRS 15 if all the following conditions are met:

- the contract has been approved by the parties to the contract;

- each party’s rights in relation to the goods or services to be transferred can be identified;

- the payment terms for the goods or services to be transferred can be identified;

- the contract has commercial substance; and

- it is probable that the consideration to which the entity is entitled to in exchange for the goods or services will be collected.

Step 2: Identify the performance obligations in the contract

A performance obligation is a promise in a contract with a customer to:

- Transfer a good or service to the customer, or

- A series of distinct goods or services that are substantially the same and that have the same pattern of transfer to the customer.

Factors for consideration as to whether an entity’s promise to transfer the good or service to the customer is separately identifiable include, but are not limited to:

- The entity does not provide a significant service of integrating the good or service with other goods or services promised in the contract.

- The good or service does not significantly modify or customise another good or service promised in the contract.

- The good or service is not highly interrelated with or highly dependent on other goods or services promised in the contract.

Step 3: Determine the transaction price

The transaction price would be the amount of consideration an entity expects to be entitled in exchange for transferring promised goods and services. In the process of making this decision, an entity will consider past customary business practices.

Where a contract contains elements of variable consideration, the entity will estimate the amount of variable consideration to which it will be entitled under the contract.

Variable consideration is also present if an entity’s right to consideration is contingent on the occurrence of a future event.

The standard deals with the uncertainty relating to variable consideration by limiting the amount of variable consideration that can be recognised. Specifically, variable consideration is only included in the transaction price if, and to the extent that, it is highly probable that its inclusion will not result in a significant revenue reversal in the future when the uncertainty has been subsequently resolved.

However, a different, more restrictive approach is applied in respect of sales or usage-based royalty revenue arising from licences of intellectual property. Such revenue is recognised only when the underlying sales or usage occurs.

Step 4: Allocate the transaction price

For a contract that has multiple performance obligations, an entity shall allocate the transaction price to the performance obligations in the contract by reference to their relative stand-alone selling prices. If a stand-alone selling price is not directly observable, an entity will need to calculate it (refer to the approaches on the right).

Occasionally the transaction price may include a discount. Any overall discount is allocated between the performance obligations on a relative stand-alone selling price basis. In certain circumstances it may be appropriate to allocate the discount to some but not all of the performance obligations.

Step 5: Recognise revenue when a performance obligation is satisfied

An entity will recognise revenue when (or as) it satisfies a performance obligation by transferring a promised good or service to a customer, which is when control is passed, either over time or at a point in time.

Control of an asset is defined as the ability to direct the use of, and obtain substantially all of the remaining benefits, from the asset.

An entity recognises revenue over time if one of the below criteria is met:

- The customer simultaneously receives and consumes the benefit provided by the entity as the entity performs

- The entity’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced

- The entity’s performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for the performance completed to date

For a performance obligation satisfied over time, an entity would select an appropriate measure of progress to determine how much revenue should be recognised as the performance obligation is satisfied.

Factors which may indicate that control is passed at a point in time include, but are not limited to:

- The entity has a present right to payment for the asset

- The customer has legal title to the asset

- The entity has transferred physical possession of the asset

- The customer has significant risks and rewards related to the ownership of the asset; and

- The customer has accepted the asset.

Contract Costs

Incremental costs of obtaining a contract

The incremental costs of obtaining a contract must be recognised as an asset if the entity expects to recover those costs. However, those incremental costs are limited to the costs that the entity would not have incurred if the contract had not been successfully obtained A practical expedient is available, allowing the incremental costs of obtaining a contract to be expensed if the associated amortisation period would be 12 months or less.

Costs to fulfil a contact

Costs incurred to fulfil a contract are recognised as an asset if and only if all of the following criteria are met:

- The costs relate directly to a contract

- The costs generate or enhance resources of the entity that will be used in satisfying performance obligations in the future

- The costs are expected to be recovered.

The asset recognised in respect of the costs to obtain or fulfil a contract is amortised on a systematic basis that is consistent with the pattern of transfer of the goods or services to which the asset relates.

Presentation

Contracts with customers will be presented in an entity’s statement of financial position as a contract liability, a contract asset, or a receivable, depending on the relationship between the entity’s performance and the customer’s payment.

A contract liability is presented in the statement of financial position where a customer has paid an amount of consideration prior to the entity performing by transferring the related good or service to the customer.

Where the customer has not yet paid the related consideration for the transfer of a good or service, a contract asset or receivable is presented in the statement of financial position. Contract assets and receivables together with any impairment shall be accounted for in accordance with IFRS 9 Financial Instruments. The difference between the initial recognition of a receivable and the amount should be presented as an expense.

Disclosure

The disclosure objective stated in IFRS 15 is for an entity to disclose sufficient information to enable users of financial statements to understand the nature, amount, timing and uncertainty of revenue and cash flows arising from contracts with customers. Therefore, an entity should disclose qualitative and quantitative information about all of the following:

- Revenue recognised from contracts with customers

- The significant judgments, and changes in the judgments, made in applying the guidance to those contracts; and

- Any assets recognised from the costs to obtain or fulfil a contract with a customer.

Entities will need to consider the level of detail necessary to satisfy the disclosure objective and how much emphasis to place on each of the requirements. An entity should aggregate or disaggregate disclosures to ensure that useful information is not obscured.

Disclaimer

This IFRS Alert is prepared by I.A.S. Accounting Services Limited with the utmost care is meant to keep you abreast of developments and is intended for information purposes only. It cannot be regarded as a binding legal, financial, tax or any other advice. Clients receiving this IFRS Alert should take no action before liaising with their I.A.S. Accounting Services Limited.

The information contained in this IFRS Alert is reflecting publicly available information as at the date of issue of this report. The reproduction of this report in whole or in part in any way, including the reproduction in summary form and the reissuance in a different manner are strictly forbidden and are only allowed with the prior written consent of I.A.S. Accounting Services Limited.